The past quarter in financial markets has seen moderate investment returns for the broader Australian Equities market, while its International counterparts performed materially better. This continued market and investment return volatility looks like the new ‘norm’ for now.

In an attempt to maximise the current market backdrop, Financial Keys recently caught up with Perpetual to discuss the merits of investing into what we call a Long / Short investment vehicle.

Alpha is the outworking of a Fund Manager’s stock picking skills. It is the ability to add value above the market.

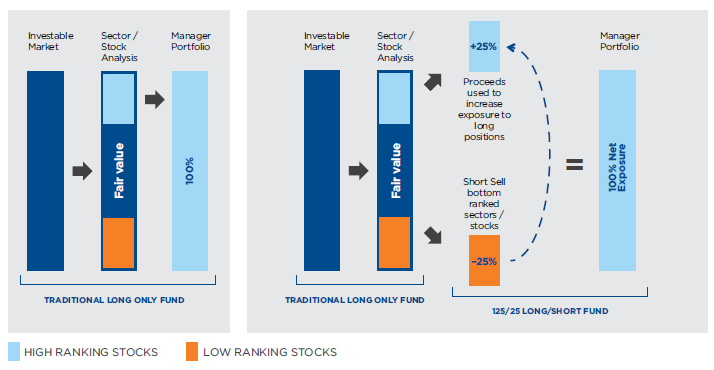

A Traditional Long Only Fund

Fund managers analyse an investable universe created according to certain investment criteria, ie sound management, quality of business, conservative debt and recurring earnings. They then rank stocks on valuation metrics. The highest ranking stocks are included in the portfolio; nothing is done with the low ranking stocks.

Long/Short Fund: Increasing The Opportunity For Alpha

Fund managers employ teams of analysts to evaluate risks and opportunities, good news and bad news. The majority do nothing with the bad news, other than avoid certain stocks.

The combination of a long/short fund provides investors a way to profit from the bad news, as well as the good.

A long/short fund allows a fund manager to actively utilise the low ranking stocks by shorting them. This can increase alpha in a combination of different ways:

These opportunities are particularly valuable in volatile or sideways trading markets.

Why Risk Management Is Important

When an investor buys a share, the worst case outcome is that he or she loses all the money they paid for it. However, when an investor shorts a share, the theoretical risk is limitless because the share price of the company could increase forever.

At Perpetual, we believe that shorting requires a specific skill set and a prudent risk managed process in order to achieve a favourable balance of risk and return for investors.

While well-chosen short positions can generate returns, especially during periods of market uncertainty, taking short positions does involve higher levels of risk than taking long positions only.

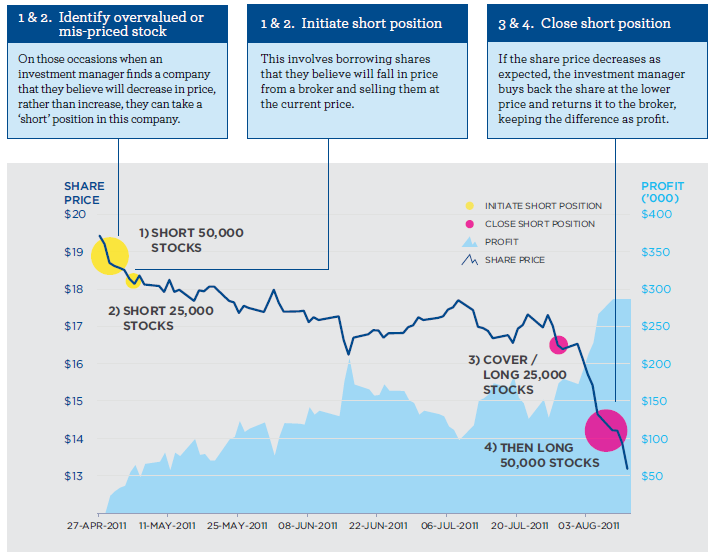

Profiting from a falling share price takes a unique stock picking skill. This example demonstrates how it works in practice.

Key Benefits of Shorting

While shorting strategies have the potential to generate returns in both up and down markets, there are a number of myths about shorting that have stopped many investors from using these strategies within their portfolios.

1. Shorting can make a company go bankrupt

Shorting a share is no more sinister than selling a share for less than you paid for it. Assuming a company has a reasonably strong balance sheet, even if its share price fell to zero, it would still be worth the value of its balance sheet. All shorting does is expose weak companies.

2. Shorting played a part in the GFC

Prior to the global financial crisis (GFC), there were a lot of companies with overstretched balance sheets and these were exposed during the GFC. Shorting did not create the downward pressure on these shares during the GFC. However during the extraordinary circumstances of the GFC, it can be argued that it compounded the pressures already at play.

3. Shorting = Positive Returns

While shorting provides the opportunity to profit in both rising and falling markets, not all short positions generate a positive return. In fact, shorting is a specialist skill, as picking companies that will decline in price can often be much harder than picking companies that will rise in price.

4. Shorting is not transparent

All short selling transactions and positions are declared to the Australian Securities Exchange at the end of each trading day and are available to all market participants.

5. Shorting is not ethical

Some view shorting a company as tantamount to wanting it to fail. This is not the case. In fact, shorting can be a benefit to the overall market because it adds liquidity, improves trading efficiency and helps to highlight where poor company management is not delivering on its promise to shareholders.

6. Shorting involves unlimited downside risk

It is true that, when opening a short position, the theoretical risk is limitless because the price of the share could increase forever. However, a ‘stop loss’ (see right) is used by prudent managers as a risk control tool to limit the loss if a short position rises instead of falls in price.

7. Shorting doesn’t work

The positive long-term performance of market indices leads many to believe that shorting does not work. The aim of short selling is to profit from shorter-term factors, such as negative news or earnings downgrades, and can be used as a complement to a long portfolio that benefits from share price gains over the long term.

Risk Management: A Stop Loss

Having a rigorous risk management process in place is a key part of any successful shorting strategy. The process we use for all our long-short strategies is:

Together, these risk controls mean that the worst possible portfolio impact of a single poor short position is a negative 0.25% return for the portfolio.

Global markets delivered mixed but generally resilient outcomes over the December quarter, as investors navigated shifting expectations for interest rates, valuation pressures and ongoing geopolitical uncertainty. Early volatility gave way to steadier conditions toward year end, supported by the US Federal Reserve’s December rate cut and continued confidence in corporate earnings. Artificial intelligence remained a key structural theme, while strength in defensive sectors, commodities, and gold helped balance a more selective risk appetite.

2025 unfolded against a backdrop of heightened geopolitical tensions, shifting central bank policy, and uneven global growth. Markets began the year cautiously, with Donald Trump’s return to the US presidency renewing tariff uncertainty and contributing to early volatility as investors assessed potential impacts on trade, inflation and corporate earnings. Confidence gradually improved as inflation moderated across major economies and expectations for steadier policy settings emerged. A powerful theme in markets was the accelerated investment in artificial intelligence, which became a central driver of global market leadership as the year progressed.

Global markets surged in the September quarter of 2025 driven by optimism around monetary easing and A.I. innovation alleviating earlier concerns over tariffs and slowing growth. Global equities powered higher on a wave of strong earnings, a long-anticipated US rate cut, and continued enthusiasm for A.I. Commodity and credit markets also strengthened, while volatility briefly flared around policy uncertainty and fiscal stress, particularly in Europe, amid a looming US government shutdown.