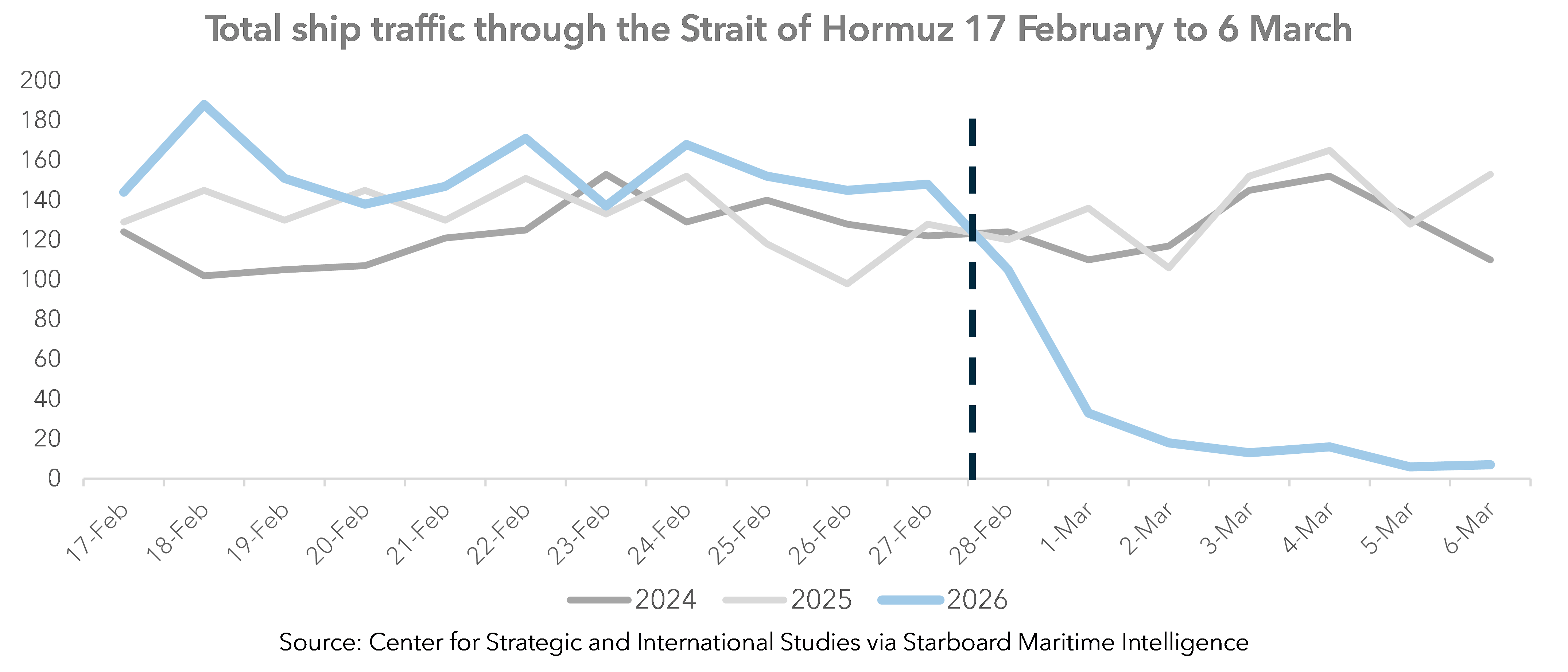

The quarter began with positive sentiment, supported by resilient growth, rising share markets and firm commodity prices, while fixed interest remained subdued as bond yields rose early in the period before declining in February. Sentiment shifted in March as confidence weakened amid escalating conflict in the Middle East, disrupting shipping flows through the Strait of Hormuz (see chart below), raising concerns around oil supply, lifting oil prices and the inflation outlook, with markets becoming more volatile as uncertainty increased.

Australia’s reliance on imported fuels, sourced largely from Asian refineries dependent on Middle Eastern crude, amplified the impact. Disruptions to fertiliser supply chains, where a meaningful share of imports is sourced via the Persian Gulf, added further pressure, lifting input costs across the broader economy. Together, these factors drove higher energy and production costs, weighing on more cyclically exposed sectors, while real assets such as infrastructure continued to demonstrate relative resilience.

Looking ahead, the investment landscape has become more complex, with a more cautious stance emerging as the earlier expectation of gradually falling inflation and near-term interest rate cuts is being challenged. The re-emergence of energy-driven inflation, combined with geopolitical uncertainty and structurally higher government debt, points to a more conditional path for central banks. Inflation risks remain material, valuations in parts of equity markets are elevated, and credit spreads remain tight relative to history despite widening more recently, supporting a more balanced and selective approach.

In this environment, selectivity is important, with a focus on managers and strategies exposed to companies with attractive valuations, broadening earnings and lower sensitivity to higher energy costs. Infrastructure, where revenues are often linked to inflation and supported by stable, long-term cash flows, offers more stability in an uncertain environment. Within fixed interest, higher quality exposures and domestic duration continue to offer stability in more volatile conditions, while credit warrants a more selective approach.

Despite heightened market volatility, the foundations for long-term growth remain firmly in place. Investment in AI continues to support productivity and earnings, while periods of volatility are opening up opportunities across regions and sectors. Maintaining a disciplined, diversified approach focused on quality and resilience remains central, with portfolio decisions grounded in long-term fundamentals and implemented with patience as conditions evolve.

As we have reached the end of another financial year, we wanted to send a reminder about income distributions.

Last night’s Federal Budget has created debate and discussion and much has been published regarding this budget which contains significant changes.

Global markets delivered mixed but generally resilient outcomes over the December quarter, as investors navigated shifting expectations for interest rates, valuation pressures and ongoing geopolitical uncertainty. Early volatility gave way to steadier conditions toward year end, supported by the US Federal Reserve’s December rate cut and continued confidence in corporate earnings. Artificial intelligence remained a key structural theme, while strength in defensive sectors, commodities, and gold helped balance a more selective risk appetite.